There is a very specific type of person who got rich from the British pub trade in the 1990s and 2000s.

They were not publicans. They were not brewers. They had never pulled a pint in their lives, and many of them had no intention of ever doing so. They were financiers, private equity operators, and investment bankers, and they spotted something that the 1989 Beer Orders had inadvertently created: a captive market of tens of thousands of tied tenants, locked into contracts they couldn’t easily escape, paying above-market prices for beer to landlords who answered not to the communities their pubs served, but to bondholders and hedge funds.

Running this problem at your pub?

Here's the system I use at The Teal Farm to fix it — real-time labour %, cash position, and VAT liability in one dashboard. 30-minute setup. £97 once, no monthly fees.

Get Pub Command Centre — £97 →No monthly fees. 30-day money-back guarantee. Built by a working pub landlord.

What followed was one of the most consequential and least understood financial engineering operations in British corporate history. And when the model eventually broke, as all debt engines do, it was the pubs and the people inside them who paid the price.

The Men Who Saw the Opportunity

In 1994, Guy Hands joined Nomura International, where he established the Principal Finance Group a division dedicated to acquiring and restructuring underperforming assets using the bank’s balance sheet. PFG specialised in opportunistic purchases of distressed or poorly managed entities, including UK pubs, financed through cash-flow-backed securitisations. Under Hands’ leadership, the group executed pioneering deals, including early securitisations in the pub sector starting in 1995, which demonstrated the viability of leveraging non-traditional assets to achieve high returns. Grokipedia

Read that again carefully. Pubs, community assets, and social infrastructure, where people had been meeting for centuries, were being reclassified as “non-traditional assets.” The question being asked was no longer “What does this pub do for its community?” The question was: how much cash flow can we extract from this building, and what can we borrow against it?

Those at the helm of the new pubcos had little, if any, connection to the sector and very little empathy for it. Everyone wanted a piece of the action, piling in to make money with little interest in the pubs, the people who ran them, the communities that used them, or the wider economic impact. UK Parliament

This was not a secret at the time. It was the business model, stated openly.

The Mechanics of the Debt Engine

To understand what happened next, you need to understand how securitisation works in this context because it is the mechanism that turned the British pub estate into a financial instrument.

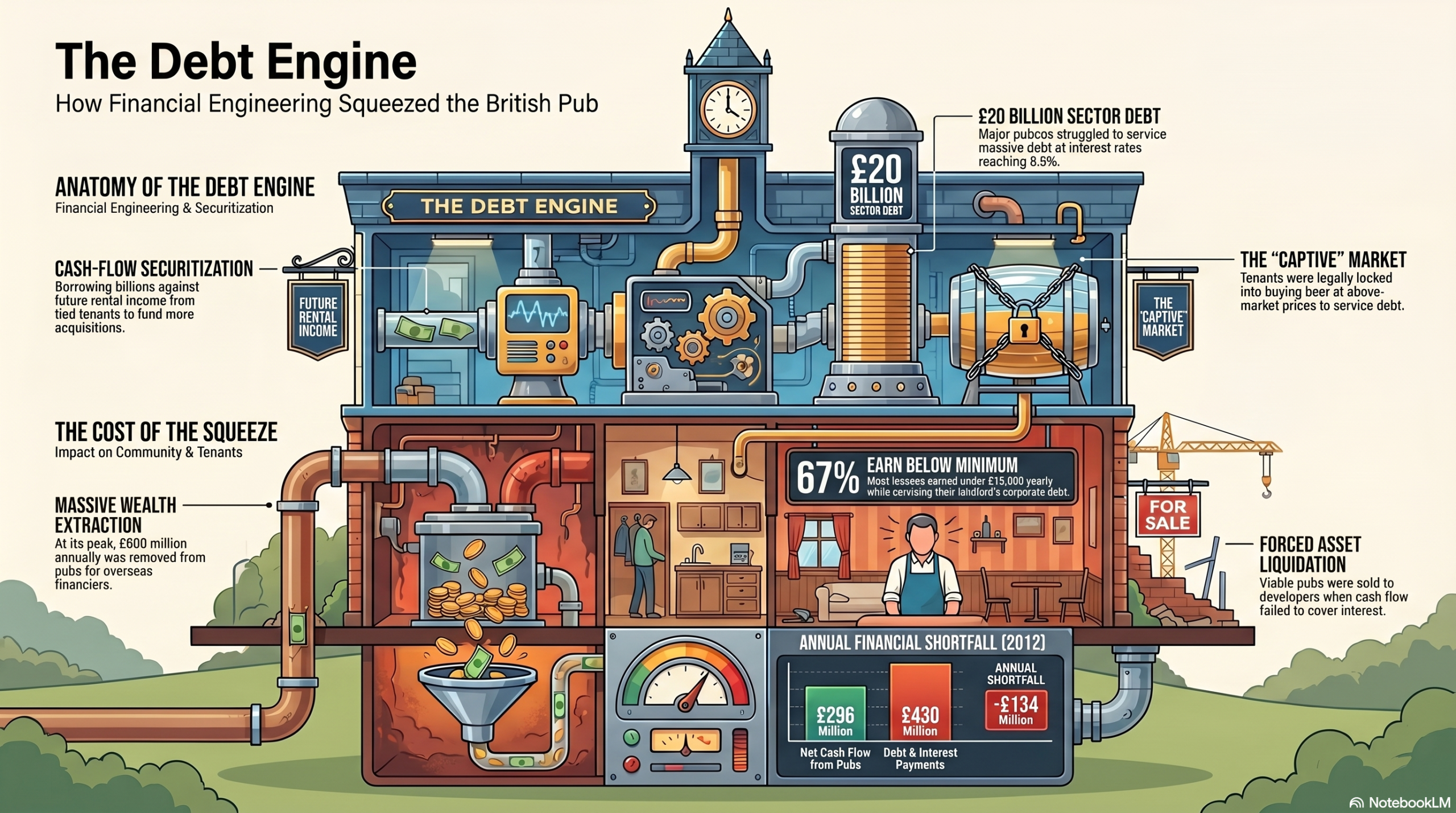

The pubcos borrowed enormous sums of money, secured against the future rental income from their tied tenants. They used that borrowed money to acquire more pubs. More pubs meant more rental income. More rental income meant they could borrow more. They used that to buy still more pubs. The engine fed itself, as long as rents kept rising and tenants kept paying.

Aided by investment bankers, pubco bosses produced financial models and projections that assumed practically perpetual growth in the rents and beer prices they could charge their captive market of tied licensees, who would be unable to resist such aggressive pricing strategies. UK Parliament

The word “captive” is doing a lot of work in that sentence. Tied tenants couldn’t simply walk away. They had signed leases. Many had invested their life savings in fixtures, fittings, and goodwill. Their homes were often above the bar. The pubco knew this. The financial model depended on it.

At the peak of the madness, as much as £600 million a year was being removed from UK pubs and paid, much of it overseas, to hedge funds in the US and other debt providers. Larry Robbins of the $7 billion fund Glenview Capital Management described Punch Taverns’ hapless tenants as the source of ever more money for Punch and his fund. TheyWorkForYou

There it is, from the horse’s mouth. British publicans running community pubs, paying into local economies, often living on the premises described by an American hedge fund manager as a “source of ever more money.” Not partners. Not operators. A revenue stream.

The Scale of What Was Built

The numbers are staggering.

Together, Punch and Enterprise alone owned 16,000 pubs at their peak. There was around £20 billion of debt in the sector overall. Both Enterprise and Punch were struggling to service debt of approximately £8.5 billion between them, requiring together around £730 million a year just to meet their debt obligations. brauwelt

Punch and Enterprise were trying to cut debt built up through acquisitions during the boom years of the 1990s and early 2000s, before the recession. With securitised money washing through the pubcos, all that was left was a largely debt-ridden sector paying interest rates of up to 8.5% on billions of pounds. International Business Timesparallelparliament

Consider what this meant in practice for a tied tenant. Their landlord, the company they were legally obligated to buy their beer from at above-market prices, was simultaneously trying to service billions in debt at 8.5% interest and had financial models built on the assumption that rent and beer prices would rise indefinitely. The tenant had no leverage, no meaningful right of appeal, and in many cases, no independent legal advice when they signed.

In 2012, Enterprise had a net cash flow from its pubs of £296 million — but in the same year its debt and interest payments totalled £430 million. As a result of this £134 million shortfall, the company was selling off pubs regardless of the interests of pubgoers and their communities. Protzonbeer

The maths had become impossible. And rather than restructure the business model, the pubcos did what over-leveraged property companies always do: they sold assets. The assets, in this case, were pubs. Often perfectly viable pubs. Often in communities where the pub was the last public meeting place for miles.

Parliament Noticed. Nothing Changed.

Here is where the story becomes genuinely scandalous, because what happened next was not ignorance. It was knowledge, deliberate inaction, and repeated failure to act.

A unanimous 2009 Business and Enterprise Select Committee report raised serious questions about the pubco-tied pub business model and called on the government to act urgently, recommending the matter be referred to the Competition Commission. The committee was astonished to learn that 67% of lessees surveyed earned less than £15,000 a year, and over 50% of lessees with turnover of more than £500,000 a year still earned less than £15,000, a 3% rate of return. The lessees may share the risks with their pubco, but they do not appear to share the benefits. UK Parliament

The committee also found a worrying pattern in the evidence of lack of support for lessees, verbal agreements not honoured, and, on occasion, downright bullying. UK Parliament

The select committee was not generally impressed by the pubcos’ senior executives, rebuking them for having given partial and even false evidence. UK Parliament

Executives lied to Parliament. The committee said so explicitly. The government’s response was to ask the pubcos to regulate themselves, a process that had been failing since 1998 and would continue to fail for another decade.

A self-regulatory approach had been in operation since at least 1998, but it was found wanting by the Select Committee in 2011 and the government in 2012. Six revisions of the Framework Code were published but none of them made any attempt to ensure an equitable split of profits between licensees and pubcos. The Chief Executive of the BBPA said “it is not the role of the BBPA to look at tenants’ profit.” Wikipedia

There is the trade association representing the industry, stating openly that what tied tenants actually earn is not their concern. While their members were paying 8.5% on billions of borrowed pounds, and passing the cost down the chain to publicans taking home less than £15,000 a year.

The Pubs Code: Too Little, Too Late, and Mostly Ignored

A statutory Pubs Code finally arrived in 2016, introducing the Market Rent Only option, allowing tied tenants to break free of the beer tie at certain trigger points and pay a market rent instead. The principle was sound: tied tenants should be no worse off than if they were free of tie. Morning Advertiser

The practice has been a different story.

During Covid, pubcos chose to interpret the code differently for tied tenants than for free-of-tie tenants, charging tied tenants full rent during lockdown. Anyone who had taken the legal right the committee suggested they had was discriminated against and charged full rent while unable to trade. UK Parliament

The first Pubs Code Adjudicator served his entire term with no visible effect. He was an estate agent with a director’s loan outstanding to one of the biggest property survey firms throughout his entire appointment, one of the clearest conflicts of interest imaginable. UK Parliament

Reform arrived. The people appointed to enforce it were drawn from the same world the reform was designed to regulate. The outcomes speak for themselves.

Who Got Out — and How

The final chapter of the pubco empire story is worth telling because it perfectly illustrates who this system was actually designed to serve.

Guy Hands seduced Giles Thorley into running Unique Pub Company just as it was being sold to Enterprise. Hugh Osmond then poached Thorley to Punch Taverns. As the share price was pumped in 2010, Thorley, clearly seeing the writing on the wall, sold out and made his fortune. UK Parliament

The men who built the debt engine, loaded it with borrowed money, and extracted billions from tied tenants, they got out. They took their money. They moved on to the next deal. Larry Robbins at Glenview Capital collected his returns and presumably found other sources of “ever more money.”

The tied tenant in the pub on the corner, having invested their savings, having worked seven days a week, having subsidised their pub income with a second job, they were the ones left in the wreckage.

Together, Enterprise Inns and Punch Taverns got rid of a third of their pub estate in just four years. Most of these pubs were sold to supermarkets and developers for alternative use, often with strong opposition from local people. Many of these pubs could have been successful under a different, fairer business model, but with the pubcos too indebted to change, only the government could step in. PUBlicity

The government, having watched this play out over fifteen years of select committee reports, parliamentary debates, and evidence of systematic failure, responded with a Pubs Code that pubcos immediately found ways around.

I have spent fifteen years inside this system. I have sat across a table at rent reviews and understood with complete clarity that the person opposite me was not there to assess a fair rent; they were there to maintain the yield that serviced a debt I had no part in creating. I have watched neighbours leave viable pubs, driven out not by failing trade but by the arithmetic of the tie.

What has happened to the British pub is not complicated. It is not mysterious. It is not cultural.

It is the predictable outcome of allowing a captive market of small operators to become the financial shock absorbers for billions of pounds of recklessly accumulated corporate debt — while Parliament watched, reported, tutted, and moved on.

Running your pub on gut feel?

The Pub Command Centre gives you wet GP%, cellar checks, staff cost and weekly P&L — from your phone, every shift. £97 once. No subscription.

See the Pub Command Centre →